U.S. government bond yields declined today, continuing yesterday's drop, indicating an increased demand for defensive assets, which is also confirmed by the weakening dollar against other popular defensive assets such as the yen, gold, and franc. Meanwhile, the dollar index (DXY) also resumed its decline after a tentative rise earlier this week.

Still, market participants ignore the Fed's intention to continue tightening its monetary policy. The focus here is not that the Fed's interest rate will rise, but at what pace and in what amounts. The fact that the Fed's leaders plan to raise the interest rate at the meeting on January 31 and February 1 no longer suits dollar buyers. They expect the Fed to continue aggressively tightening policy, and this, perhaps, will not happen. The most likely will be to raise the interest rate at the next meeting by 0.25%, and then the option is not ruled out that the Fed leaders will take a break, and then they can completely switch to policy easing.

This may be prompted by the recent U.S. inflation data. Yesterday's report by the U.S. Bureau of Labor Statistics pointed to another slowdown in manufacturing inflation: the producer price index fell in December (to -0.5% against the forecast of -0.1% and the previous value of +0.2% and to 6.2% in annual terms against the forecast of 6.8% and the previous value of 7.3%). Last week, consumer inflation data also showed another slowdown, with the annual CPI dropping back to 6.5% in December from 7.1% a month earlier and core CPI dropping to 5.7% from 6% in November.

At the same time, data on some of the most important sectors of the U.S. economy show a slowdown, which is a consequence, among other things, of the Federal Reserve's tight policy.

In particular, according to yesterday's data, the volume of industrial production declined again to -0.7% in December from -0.6% in November, stronger than the forecasted -0.1% decline, while the capacity utilization rate decreased to 78.8% from 79.4% a month earlier.

Despite the fairly good labor market conditions, the above and other data put pressure on Fed policymakers to reconsider their tough approach to monetary policy parameters in the direction of easing. Raising rates when macro economic indicators deteriorate is an unacceptable mistake, economists say, specially since the Fed's tight monetary policy has already borne fruit—inflation is declining, although it is still far from the 2% target level.

Today, market participants will receive new information and food for thought on the Fed's monetary policy outlook. At 13:30 (GMT), the U.S. Bureau of Labor Statistics will publish weekly data from the U.S. labor market. Jobless claims are expected to rise. Although the labor market remains strong and unemployment is at pre-pandemic lows, the rise in jobless claims is a negative for the dollar.

As for the euro, it is growing in pair with the dollar and in major cross pairs.

Investors are still optimistic about the euro outlook amid expectations of another ECB interest rate hike and verbal interventions of its representatives.

Speaking at the World Economic Forum in Davos today, ECB President Christine Lagarde said that "inflation expectations are not easing" and "the ECB will continue to raise rates." In her opinion, "inflation is too high," and "the ECB intends to bring it down to 2% in a timely manner."

Lagarde will give another speech tomorrow starting at 10:00 (GMT). Until then, the euro will probably maintain the bullish momentum from today's remarks.

Next week, a whole block of macro statistics from the Eurozone will be published. In particular, fresh data on business activity in key sectors of the German and European economies will be presented on Tuesday. A decline in European PMIs is expected, which should have a negative impact on the euro, especially since the indices are still below the 50 mark separating the growth of activity from its slowdown.

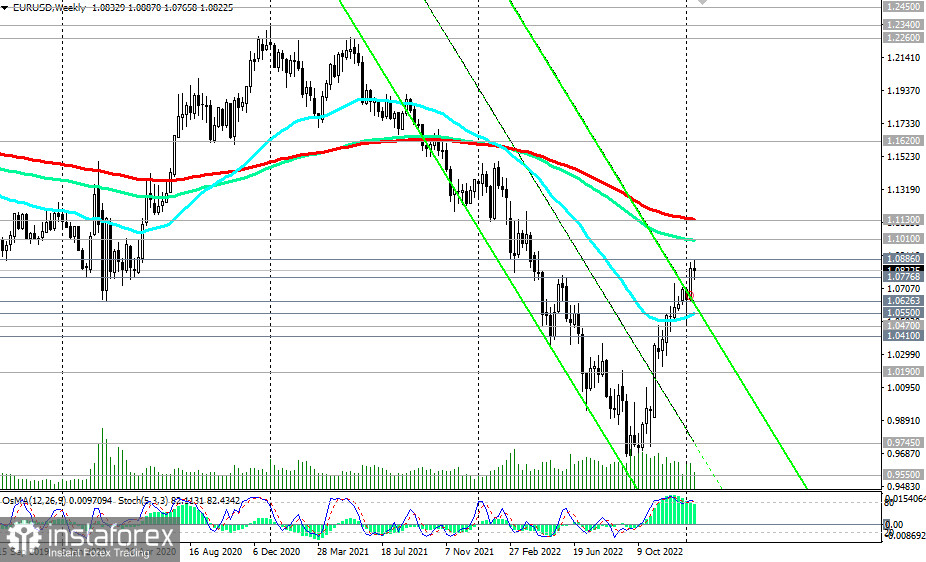

As of writing, EUR/USD was trading near 1.0822 after reaching a new local and 9-month high of 1.0886 yesterday. Despite this decline, a strong bullish momentum remains, pushing the pair towards the key resistance levels 1.1010, 1.1130, separating the pair's long-term bullish trend from the bearish one. Thus, long positions remain preferable.