Every day in the UK alone, about 1.4 billion pounds ($1.9 billion) are pumped through loosely regulated digital payments companies such as Moorwand. Although this is only a small part of the UK's financial flows, many experts warn that this opens the door to dirty money.

Do you use electronic payment systems? Choose carefully

The Moorwand company is one of more than 200 electronic money institutions, or EMI, approved by UK regulators since 2018. Almost immediately after the start of the institution's activities, problems followed: a tiny lender in Denmark, with whom Moorwand had established a close relationship, reported hundreds of suspicious transactions involving a payment firm. In the same year, in the same case, the Danish authorities arrested the Kobenhavns Andelskasse bank, citing violations of the law on money laundering, and referred the case to the police.

However, Moorwand, controlled by Moldovan businessman Wael Sulaiman Almaree, has not been charged with any wrongdoing and still has the power to transfer client funds. Neither Almaree nor Moorwand responded to repeated requests for comment.

From 2017 to early 2020, the use of e-money accounts quadrupled to 4% of the adult population. The Bank of England, which does not regulate e-money companies, claims that customers have about 10 billion euros ($ 11.3 billion) parked at such companies.

Now, questions are gradually being raised again regarding dozens of such EMI institutions that have received a license thanks to the efforts of the authorities to enhance London's reputation as a center of financial technology and revive competition in the banking sector. At the same time, hundreds of regulatory, legal and corporate documents paint a rather disturbing picture of this corner of the market. And they point to weaknesses in the supervision of the UK Financial Supervision Authority. So, among the companies approved by the FCA, there are companies whose managers or shareholders are associated with money laundering scandals in the Baltic States, alleged financial offenses in Russia and Kyrgyzstan, healthcare fraud in the United States and suspected offenses in Luxembourg and Australia. Dozens of firms are controlled by investors in jurisdictions far beyond the UK, including the British Virgin Islands, Cyprus, Ukraine and the United Arab Emirates. Some openly brag about doing business with high-risk clients.

Transparency International UK, the UK arm of the global anti-corruption group, sounded the alarm in its report last month, saying that more than one-third of FCA-licensed EMIS have red flags related to their activities or owners/directors.

"This is the Wild West, even without the additional complications associated with those who master this segment with deliberate criminal intentions," said Graham Barrow, a financial crimes analyst who has worked for lenders such as HSBC Holdings Plc, Nordea Bank Abp and Societe Generale SA. "What you have is in free circulation, and regulators are desperately fighting to catch up with it."

The FCA data shows that the agency has taken certain actions. Last year alone, it rejected 50 out of 89 applications, having also conducted eight official EMI inspections. The regulator has previously imposed restrictions on doing business with respect to four more firms.

"We are focused on fighting financial crimes," an FCA spokesman said in an email, declining to comment on Moorwand or other suspicious financial entities. - We have done a significant amount of work to improve the standards of combating financial crimes in companies dealing with payments and electronic money, including the introduction of restrictions on doing business for some of them. We will continue to take decisive action in cases where firms do not meet the standards we expect."

A bit of history

EMI appeared about ten years ago. They offer payment services such as transaction processing, prepaid cards, international money transfers, and digital wallets. But they often serve high-risk clients that traditional lenders refuse to deal with, such as those who trade cryptocurrencies, said John Wedge, a partner at London-based accounting firm Berg Kaprow Lewis LLP.

"These guys (cryptocurrency owners - author's note) can't use banking services," said Wedge, who works with payment companies. "What they (EMI – author's note) are doing now is filling a gap in the market that is not being filled by High Street banks or major acquiring banks."

According to government estimates, money laundering already costs the UK more than 100 billion pounds a year, and the spread of EMI without stricter regulation could worsen London's reputation as a dirty money center, Wedge and other financiers say.

The concern became even more serious after the collapse of Wirecard AG in Germany last year. The main regulatory body of this company, BaFin, ignored all signs that it was a one-day company. And when it exploded, funds worth $2.3 billion disappeared from accounts without a trace.

"If you were sitting in the place of someone from the FCA, you would be worried," says Alan Brener, a law professor at University College London who has studied the EMI industry. He claims that there are plenty of firms like Wirecard in England.

According to Brener, governments across Europe have been trying for years to shake up the payments business and wrest control from global banks to cut costs for customers. The European Union Directive on Payment Services, introduced in 2007 and revised about ten years later, was designed precisely to simplify transactions and encourage new market participants.

Since then, e-money companies have generally been subject to more lenient regulation than banks. They are allowed to process payments and store customer funds, but customers are not protected by national deposit insurance programs, and firms cannot provide loans.

More reputable firms, including Revolut Ltd. and Checkout.com , as well as dozens of smaller ones, are part of the growing London financial market, one of the largest in the world and highly valued by the UK government after the UK leaves the EU.

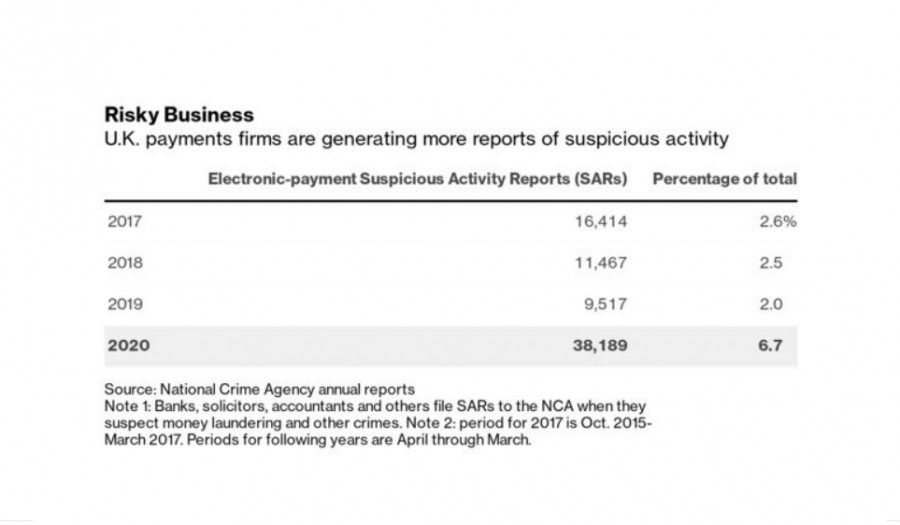

Along with the growth, there is the potential for more risk. The number of Suspicious Activity Reports (SAR) related to the electronic payments sector has quadrupled since March 2019. A spokesman for the UK's National Crime Agency has reported a sharp rise in the SAR that firms and individuals have to file when they come across it. Given the growth of the industry, we should not be surprised by the increase in the number of such reports. The Bank of England warned that in this sector "systemic risks may arise in the future."

Moorwand – a controversial story

Few people have caught more in this murky waters than former Moorwand CEO Robert Courtneidge. 57-year-old Courtneidge, known for his payment knowledge, who has been a qualified lawyer since 1990.

By the mid-2010s, he was a consultant at the American law firm Locke Lord LLP, actively participated in the awards ceremony in the field of financial technology in London and began to hold positions on the board of directors of EMI. He also advised on cryptocurrency Ruja Ignatova from Bulgaria, known as Cryptoqueen, who was then promoting the digital currency OneCoin. The U.S. attorney's office accused her of fraud for $4 billion. She never appeared in court to face charges.

In 2015, Courtneidge became a director of AF Payments Ltd., a London-based firm licensed by EMI a few years later. The founder and CEO of the company is a financial technology entrepreneur Guy Raymond El-Khoury, but, as the data show, the only registered shareholder of the company is a company from the British Virgin Islands.

El Khoury previously ran FBME Card Services Ltd., a company affiliated with FBME Bank Ltd., which is known for being excluded from the US financial system after allegations of money laundering to criminal organizations and paramilitary groups, including Hezbollah. El Khoury said through his lawyer that he was not responsible for wrongdoing in the company, and he was not involved in money laundering, but rather sought to put an end to it. Neither El-Khoury, AF Payments, nor Courtneidge have been charged with any wrongdoing.

Courtneidge joined the board of directors of CFS-ZIPP Ltd., another EMI, in 2016. According to the lawsuit, he helped arrange a loan of 1.5 million pounds from the company and its owner for a currency trading firm, which was promoted by the then business partner. This company, SwissPro Asset Management AG, went bankrupt in 2019 with losses of more than 50 million pounds. The Swiss regulatory authority said in a letter to creditors that the business is based on a Ponzi scheme, known in our country as a "pyramid". Courtneidge, who left the board of directors of CFS-ZIPP in the same year, was not accused of violations.

Instead, he became a director of ePayments Systems Ltd. in 2018, two months after that firm received an FCA license. Founded by a Russian businessman and controlled by unidentified offshore shareholders, the company has accumulated about 175 million pounds of customer funds, according to data from the UK. However, in February 2020, the company announced that it had suspended all activities following an FCA investigation into the company's money laundering. Courtneidge left the board of directors a few days later and was not accused of any wrongdoing.

But ePayments announced on its website last month that it had resumed work. Masoud Zabeti, a Greenberg Traurig lawyer representing the firm, said the company has "developed a robust and industry-leading approach to support fraud eradication and money laundering prevention."

Courtneidge declined to comment on his work at ePayments or any other company, but clarified that the EMI industry has been "transformed in recent years" in response to increased attention. "There has been a marked improvement not only in the level of understanding and implementation of the relevant rules in accordance with the FCA guidance," he said, "but also a much better ability to apply this guidance in practice."

The legislator gently lays

The FCA's 290-page guide to payment service companies describes a rigorous approval process. The candidate must be able to convince the regulatory body that its managers "have a good reputation" and have not been convicted of a crime, have not been investigated by other bodies and have not been the subject of a negative conclusion in civil proceedings. If a successful candidate then raises suspicions, the observer has broad enforcement powers, including conducting raids, probing their operations, and suspending or revoking licenses.

But having power is one thing, and using it is another. The Bank of England has warned of possible gaps in the supervision of payment companies in 2019 and called for a thorough analysis of how the industry is monitored. And the FCA was criticized by lawmakers after the collapse at the beginning of last year of the issuer of mini-bonds London Capital & Finance Plc, as a result of which retail investors suffered losses of more than $300 million.

There were no electronic payments in this case, but the subsequent investigation was put on the brakes under the then chief Andrew Bailey, now governor of the Bank of England. A spokesman for Bailey declined to comment.

In June, a parliamentary committee concluded that the FCA should set out the key stages of transforming its culture. The agency demanded the adoption of a law giving it additional powers to supervise EMI managers, which would bring its powers in line with its supervision of bank managers.

Jane Gee, a compliance lawyer who works with payment companies, said that the risks of an FCA audit are low, that the agency lacks staff to conduct investigations and that it is ineffective in combating financial crimes.

"FCA is between a rock and an anvil," Gee said. "It doesn't have enough resources, and it's also under pressure to keep the market open."

Some enforcement measures raise more questions.

For example, the London-based Allied Wallet Ltd. FCA forced it to liquidate in 2019, just 18 months after it was granted an EMI license. In May of the same year, the US Federal Trade Commission accused the company and its owner Ahmad Khawaja of processing payments for pyramid schemes, and then imposed a fine of $110 million as part of the settlement of the dispute.

In August 2021, the Massachusetts prosecutor's office accused Khawaja and others of organizing a $150 million fraud.

When FCA officials reviewed his application, Khawaja hardly had a clean record. He and the American company of the same name paid $13 million in 2010 to eliminate federal authorities' accusations of illegal processing of funds for gambling establishments. Khawaja, a fugitive from justice in a separate case, has not commented on these events to this day.

The FCA approved Moorwand's license application in April 2018, around the time Almaree took control of the company. Almaree, who was reportedly married to the daughter of former Moldovan political heavyweight Dumitru Diacov, was known for charming customers in Chisinau's best restaurants, but others were intimidated by his armed entourage, people familiar with the matter say.

Courtneidge became CEO of Moorwand in early 2018, when the company was deepening its relationship with Kobenhavns Andelskasse. Almaree became a shareholder of the cooperative bank, and Courtneidge joined the board of directors.

At that time, the bank was attracting customers from the Marshall Islands to Belize. The Danish financial regulatory authority requested a police investigation in August of the same year, noting that the lender's payment services business attracted "a large number of customers who otherwise have no natural connection with the institution" and that "such transactions are associated with a high risk of money laundering and terrorist financing."

A few weeks later, the bank was placed under the management of the Danish financial authorities. Police have since seized millions of dollars' worth of accounts linked to Almaree and Moorwand, according to reports from the Danish newspaper Borsen, which investigated the scandal. The Danish Anti-fraud agency confirmed that the investigation into Kobenhavns Andelskasse is ongoing, but declined to comment further, as did national financial regulators.

Courtneidge, who left Murwand in 2020, has not been charged with anything. And Almaree, and the company itself, too. Meanwhile, according to a review of LinkedIn profiles, key roles in the firm, including positions on risk management and customer acquisition, have been moved to Moldova.

Courtneidge remains active in the industry. He was a judge at the British Emerging Payments Awards in October, where in his red carpet interview he reflected on the problems faced by companies dealing with electronic payments. "We still have a lot going on," Courtneidge said. "Regulators are trying to fix everything."

Results

If you use electronic payment systems, try to deal with large, multinational companies that have been on the market for many years. Including because when the bubbles start to burst, all one-day firms will follow them. And it's better for your money not to be with them at this moment.