The trade war is entering an active phase, and its further escalation seems inevitable. The reason for this is another unilateral action by the United States aimed at taking advantage of a trade dispute with China, coupled with an attempt to blame what is happening on the Chinese side.

On Tuesday, the United States included China in the list of countries manipulating the national currency, and intends to achieve legitimization of its actions through the IMF mechanism, which essentially means blatant blackmail.

China, in turn, stopped buying American agricultural products, explaining this decision as a violation of previously reached agreements by the United States.

Financial markets are in a state close to chaos. S & P 500 lost 3% at the end of the bid, having dropped to 2844.1 p. But still, Asian sites are continuing trading in the red zone on Tuesday morning. The Shanghai Composite, on the other hand, decline by more than 2.5%, to 2744 p, and the Australian S & P / ASX 200 loses more than two percent. The oil quotes are also falling, while an explosive growth in bonds and gold is observed.

Why is the US so impatient? In many ways, the escalation is largely due to the fact that the reaction of the markets to the Fed decision on July 31 turned out to be insufficient, considering that inflation expectations decreased and ISM reports for July came out worse than expected.

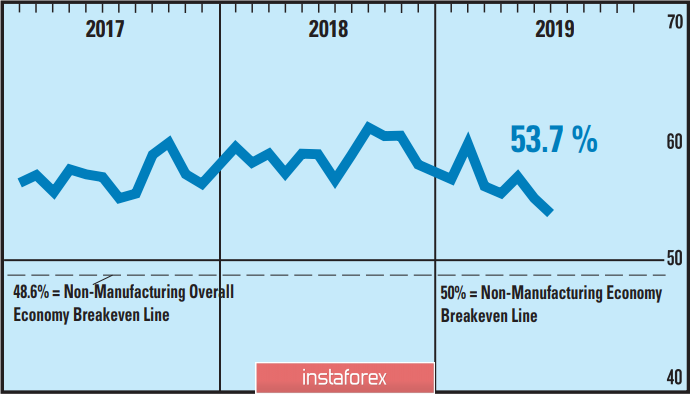

The manufacturing ISM reached the level of 51.2 p with a forecast of 52 p. For the services sector 53.7 p with a forecast of 55.5 p, both indicators are below June. The labor market report for June turned out to be neutral and generally consistent with forecasts, as well as the consumer confidence index from the University of Michigan, which has no important macroeconomic reports that are expected until the end of the week, and the state of the markets will be determined mainly by the development of the trade war.

China, in fact, has few ways to confront the United States. In order to compensate for the drop in revenue due to higher duties, the yuan rate, according to Nordea, should decline to 7.30. China is not interested in a sharp decline in its currency so as not to provoke a flight of capital, but the yuan may have no more chances to return below 7. As a result, other Asian currencies will fall, which will further increase the demand for safe assets. The point of no return may already have passed.

EURUSD

The euro has taken a short break and looks more confident, since the eurozone remains aloof from trade wars and can be perceived as a relatively safe haven at this stage. The euro is supported by the consequences of the ECB's calm decision of July 25, which declined to announce the start of a new incentive program. Moreover, macroeconomic data are neutral, which at the moment can be regarded as a positive factor for the euro.

Producer prices in June fell by 0.6%, which worsens inflation expectations. At the same time, retail sales growth was above forecasts, which offset the negative.

The composite index of Markit also shows no dynamics in any either direction. On Tuesday morning, the data on German manufacturing orders was published which were noticeably better than expected.

Therefore, the euro takes a chance and will try to strengthen on Tuesday. The immediate goal is 1.1248, the next 1.1277 / 85, and support at 1.1140 / 59.

GBPUSD

The Brexit theme is still the main concern for the pound, which prevents it from starting a recovery. According to the Guardian, the British Cabinet of Ministers does not plan to negotiate with Brussels, intends to withdraw from the EU without a deal, and return to negotiations after the exit, that is, to resolve issues of bilateral relations after the fact.

Against the background of growing fears and an escalation of currency wars, the growth of the PMI in the services sector in July from 50.2 p to 51.4 p, which could support the pound, was ignored by the markets. The pound is trading in the range, and it is slightly supported by the increased pressure on the dollar, as well as the borders of the channel 1.2080 - 1.2250, which the pound can not leave yet due to the lack of an explicit impulse. New introductory releases will appear on Friday, when an extensive data package on GDP, industrial production and trade is released.